Let’s talk about estimating your deposit and moving costs and ways to save for the most expensive purchase of your life.

Buying a home will be one and if not, the most expensive purchase you may ever make. It is important that you have enough money saved the cover the purchase and any future maintenance.

Some House Purchase Costs are:

- Deposit / Down Payment

- Solicitor/Conveyancing Fees

- Survey Fees

- Mortgage Fees

- Valuation Fees etc

“Where there is determination, you will find a way” – The Richest Man of Babylon. Let’s take a look at a few tips to help you save for the total cost of buying a home.

Government Schemes – LISA & HTB ISA

I have written a few posts about Help to Buy ISAs and LISA, please refer to those posts. In summary, there are two (2) Governments schemes HTB ISAs (now not open to new customers however, existing account holders can still use it to purchase a home) and LISA which gives account holders 25% deposit for their first home purchase.

This post includes a comparison chart between the HTBISA and the LISA.

Do not the annual limits in these accounts differs. 25% bonus on LISA are paid monthly however that for the HTBISA are paid only on redemption through your conveyancer. Refer to the brief comparison chart below.

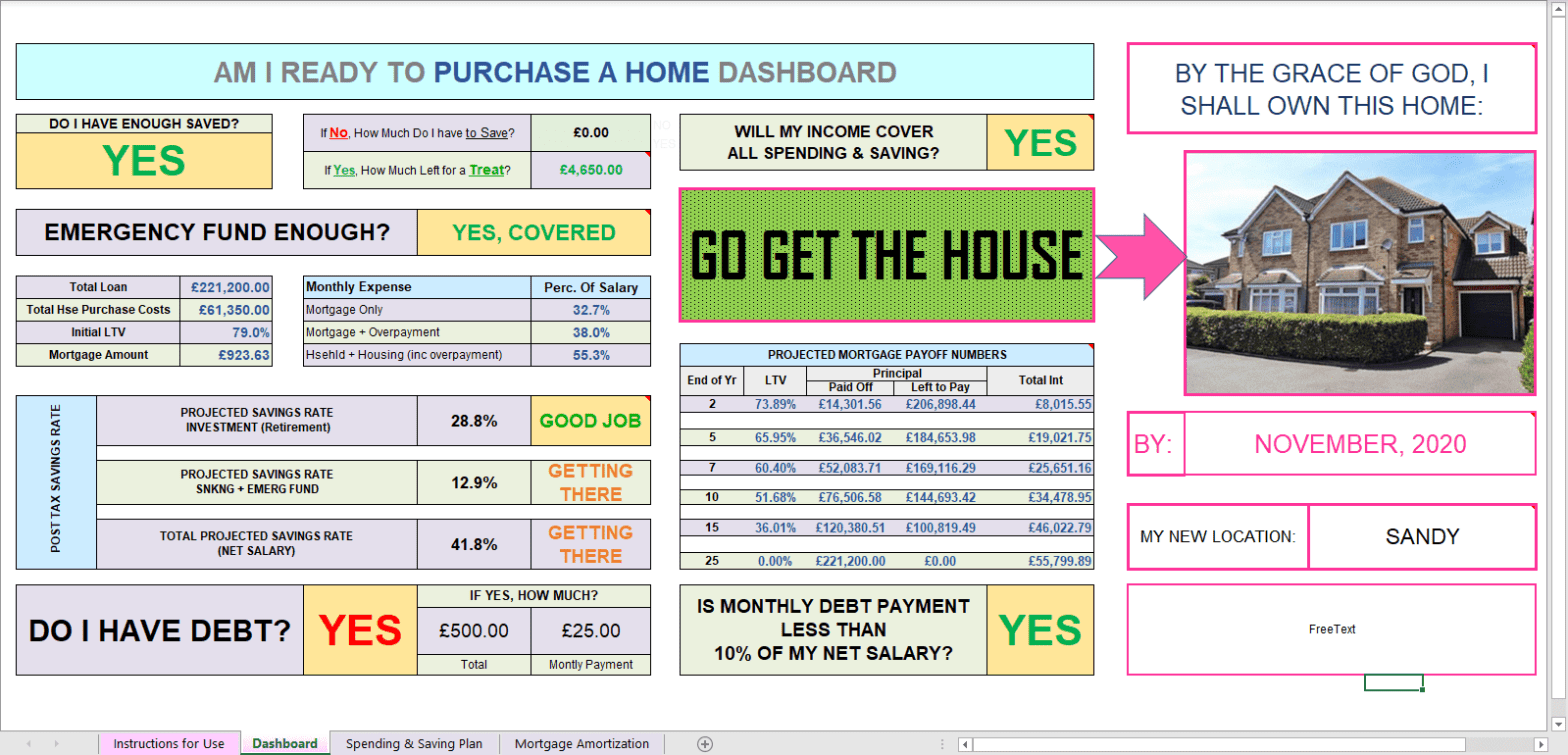

We want to help you prepare financially for your first home purchase and have provided a TOOL to help you do this. Check out:

by PrausLifeFinance

Regular Saving

We have all heard quite often to save a portion of our income (pay ourselves first). One of the effective ways to do this is to start the habit of regular savings.

Budget each month and after taking out your expenses, by direct debit contribute to a non-easily accessible savings account. I propose a non-easilt accessible savings account which prevents your from withdrawing funds. I personally use a combination of these including:

- Monthly Regular Saver (with high interest) Accounts with different banks. I don’t want to lose any savings interest.

- Account with no debit cards

- Fixed terms accounts. etc

Note: With the accounts all, especially if your are planning on buying within the next year, check to ensure there are no withdrawal penalties.

Reduce Expenses

Without increasing your income, you can consider that as a limited resource. I would encourage anyone to increase your income however, it is also a very good to reduce your expenses. Review your annual budget if you do this OR your last three statements.

For a list of some household expenses, check out this post

It is important to get rid of all unused subscriptions, reduce amount spent on eating out, debts etc. These do not only help to increase your disposable income; it also supports building new habits and making good use of your money.

The mortgage process in the UK can also be quite detailed that they will check all your outgoings to verify you can afford (although not always comfortably afford) the home.

I define comfortably affording a home as being able to pay for your mortgage with a 20% down and still managing to save and invest with no debt. If there is debt, then monthly payment should not be more than 10% of your gross salary. This is a rule of thumb I have established and not fixed. Your individual financial situation will determine this.

Check out this tool to help prepare yourself financially for your first home. It includes a dashboard which summarises atypical budget sheet, mortgage amortisation sheet etc.

Increase Income

Your rent will not necessarily be the same as a mortgage; mortgages usually come up more than rent. If they are similar, note the extra costs in owning home compared to renting especially with regards to maintenance costs (what happens if your boiler breaks down or your fridge stops working). Usually if you are in a furnished flat, the landlord/landlady will be responsible for these with allowances made for damage brought about by reasonable wear and tear.

Once you have checked the costs of owning a home or purchasing that house you have set your eyes on , it may be a good idea to use the opportunity to increase your income either by asking for a pay rise (note: each company have time frames), getting a high paid job (with same or better work-life balance) or starting a side hustle (beware of tax liabilities with side hustles).

As always, this is not financial advice; seek professional advice.