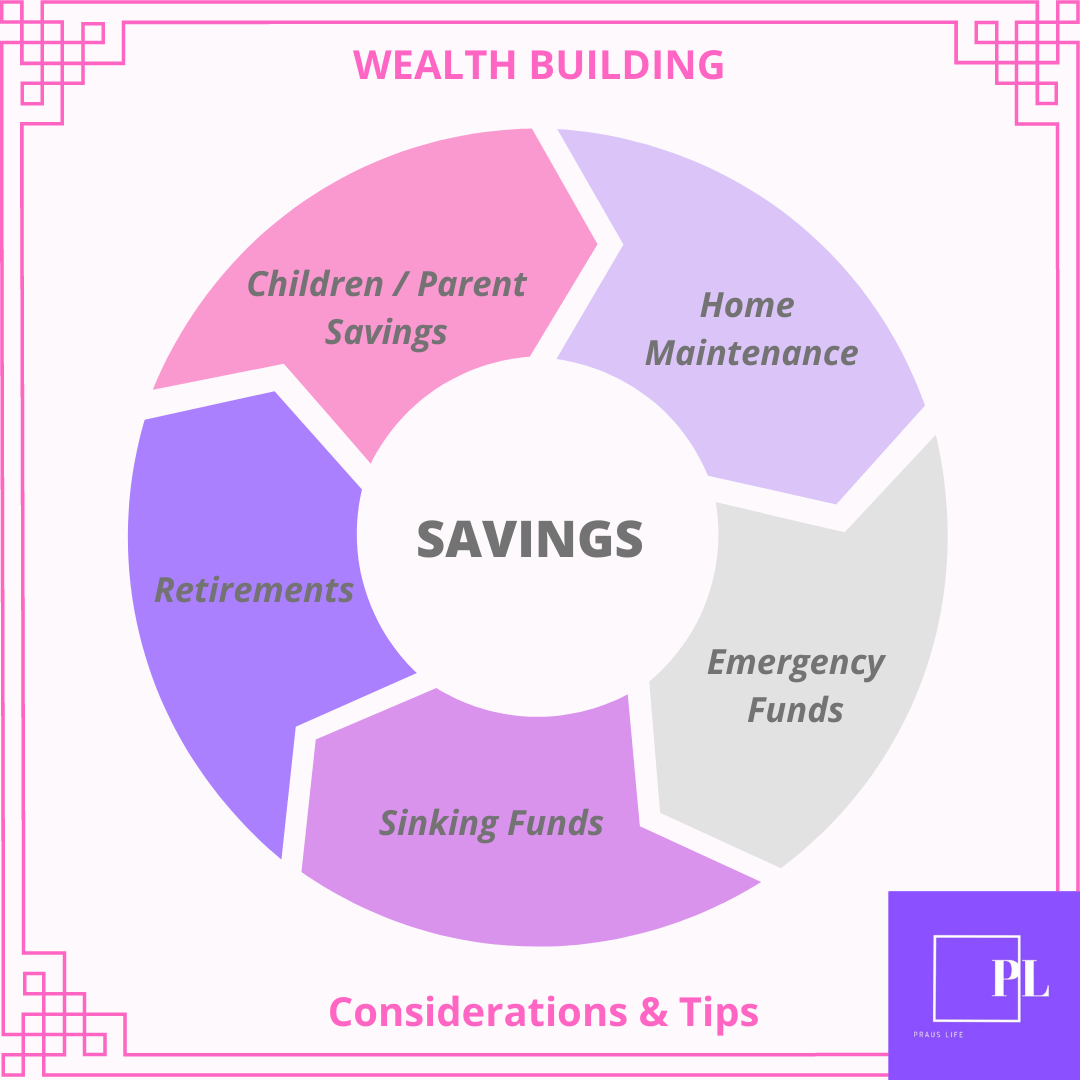

Let us talk about Savings and Investments; split into ‘savings for now’, rainy day funds and retirement. Savings = Keeping for Now and Later.

- Emergency Funds

- Retirement & Pensions

- Sinking Funds

- Home Maintenance Funds

- Children/Parent Assistance Fund

The first thing to do is to decide your goals and life aims.

Save for Emergencies & Your Future. When it Comes to Finance, Save Yourself Before Others.

Praus Life Finance

Emergency Funds

During a job loss or a time of loss of income, the Emergency Funds will cover the basic necessities of life;

- Housing – rent/mortgage, council tax, utilities etc

- Transport to work

- Communication – basic internet and mobile tariff

- Food (Groceries)

- Medical cost

After budgeting for monthly expenses each month, the first item to start saving for is an Emergency Fund.

The Emergency Fund should be enough to cover 3-6months of expenses (basic necessities). Others would ideally like to continue giving and saving and would rather save 3-6mths net salary. A person with a contract job would ideally save for a longer duration.

Each month save money into a not-so-easily accessible savings account till you achieve your EF goal.

TIP: Add up your expenses for a typical month and multiply by 3 or 6 to get your expected emergency fund amount.

Retirement & Pensions

In the world of personal finance, I believe in building your ship (looking after yourself) first. I do save for retirement and when I have kids would ensure I have saved enough or on track for a comfortable retirement prior to considering saving for my kids future.

As much as I believe in the adage and biblical verse ‘A wise man leave an inheritance for his grandchildren’, I also believe that inheritance includes not being a burden on your offspring one day. That is when retirement savings come in.

DO NOT LEAVE MONEY ON THE TABLE

My personal rules for retirement savings:

- Contribute to work place pensions. Most employers will provide a match to a maximum amount.

- Contribute to a SIPP if there are no Additional Voluntary schemes available with my Employers and/or if the fund options have very high fees or are not performing passive funds.

- Contribute to a LISA (for anyone who is less than 40 years old). Refer to the two posts at the link below for comparisons between LISAs and SIPPs.

Sinking Funds

There are things we pay for on annual basis. From car costs (insurance, maintenance, MOTs, Road Tax), House Costs (Insurance, Council Tax) to Child care, Birthdays, Christmas, Clothing, Replacing electrical items etc these are things we need to plan for. Each item is called a Sinking Pot.

In the U.K., it is usually cheaper to pay annually than monthly on car and home insurance.

We also know that Christmas comes around every year, plan for it!

How to save for a Sinking Fund

- List out all the items and expected costs

- For birthdays, decided who you are planning on giving birthday presents to. I .personally, give my nieces and nephews, a Birthday or Christmas present. They do not get both.

- Once all items and costs have been listed noting down the total amount and when each is due, divide the total by 12 (or 13 if you are paid 4 weekly) and ensure this money is saved into a separate savings account each month or pay period.

- Where particular payments dates are due before the individual pot is made ready, increase the amount saved per month (budget permitting)

- Revise the sinking pot amounts as you please.

TIP: Ensure each Sinking Pot is tracked on an excel sheet – this shows how much you have, what is left to save and what you have spent and who you spent it on.

Home Maintenance/Improvement Funds

Funds used to maintain and improve your home. In some instances, it helps to make sure that your insurances remain valid.

TIPS

1. Save an Emergency Fund.

2. Contribute to A Workplace Pension to get Employer Match.

3. Save for incidentals & annual events.

Praus life finance

For older houses, I recommend at least 2% of the home value saved in a separate pot to cover issues like roof and boiler replacement etc. I will review this figure – decrease or increase – depending on the age or updates done to the property.

Planned home renovation costs should also be saved in this pot. It is worth noting that, I would personally save an extra 15% to cover home renovation costs due to change in material costs and estimating any uncertainty.

Children / Parent Assistance Fund

Whether it is saving for children’s university tuition, contributing towards their first home, first car or even contributing towards your parents care, these are things we all want to do – either all or some.

If you have family back home or contribute towards your parents housing costs, I’d suggest just like a Sinking Fund, you calculate the annual amount and save a regular monthly amount towards this.

I think it is an honour to serve and give to our parents; do not however, do this at your detriment. Pay for your four walls, save towards retirements and then give.

Your children’s university tuition can wait. There are other options out there. For extra lessons during primary school if it is really needed, please find legal ways to cut costs some where and make extra money to cover these. Consider asking a close and trusted friend to tutor if they can whilst you offer something else in return.

Where to Keep Your Savings

Emergency Funds/Sinking Funds

Emergency Funds like Sinking Funds should be accessible however, not readily accessible like a Sinking Fund. I use a 1 year high rate savings account for my EF. These accounts assume a penalty for withdrawals however, you could find an easy access account that offers a lower interest rate to provide the benefit of a withdrawals.

Note: Emergency Funds are not an investment vehicle hence, I have not invested mine in a stock market. Even with a secure job, it is always a good thing to have it accessible.

Retirement Savings

Retirement savings through company schemes are usually held with the Pension Scheme and cannot be readily accessed and withdrawn until the Pension Age unless the rules of the fund allows it. For company schemes, please check with your Fund Administrators

Other retirement savings like SIPPs & LISAs have restrictions set by the Government on access and withdrawals from the account. Please refer to the latest government guidance on www.gov.uk.

In summary, calculate all you want to save for a year, deduct your basic necessities, save for your Emergency Fund first whilst contributing to work place pension then save for the other items.

One thought on “Keeps – Savings”